By a UK stay-at-home mum learning to build financial freedom slowly and intentionally.

Let me ask you something.

If your boiler broke down tomorrow, could you pay for it? What about a school trip letter coming home in your kid’s bag, or a car repair you weren’t expecting?

If that made your stomach flip a little — you’re not alone.

For a long time I thought saving £5 or £20 a month was pointless. Not enough to matter. So I just… didn’t bother.

I was wrong.

An emergency fund isn’t about getting rich. It’s about peace of mind. Breathing room. Having options.

I call it dignity money — because when something goes wrong and you have nothing saved, you’re either going into debt or asking someone you love to bail you out. Neither feels good.

In this guide I’ll show you how to start an emergency fund on a low income in the UK, even if money is tight right now.

I am not a financial advisor and nothing in this blog should be taken as financial advice. This content is intended for educational purposes only and is based on my own personal experience and research. Please do your own research before making any financial decisions.

Table of Contents

Why Emergency Funds Matter So Much on a Low Income

When you’re on a lower income, even a small financial surprise can feel huge.

Without savings, life starts to feel like a loop — waiting for payday, hoping nothing goes wrong, feeling like you’re always one step behind. And that kind of stress wears you down quietly, in ways you don’t always notice.

For me it stopped being about money and started being about security. Because when you have even a small buffer, something shifts. You’re less panicked. Less dependent on others. Less trapped.

You stop feeling like one unexpected bill could undo everything.

And if you’re a parent? That feeling matters even more.

The Biggest Reason Most People Never Start Saving

One of the biggest reasons people never start an emergency fund is because they believe they don’t earn enough for it to matter.

They look at £5 or £20 and think — what’s the point?

So they never begin.

But here’s what I wish someone had told me earlier: the amount matters far less than the habit.

Even £3. Even £5. Even £10.

Because at the beginning you’re not building wealth. You’re building the identity of someone who saves. And once that starts, something quietly shifts. You start noticing small amounts you didn’t notice before. You get more intentional. You feel a little less out of control.

Small amounts don’t look impressive today. But neither does a seed.

Step 1: Know Your Numbers

Before you can save more money, you need to know where your money is currently going.

Sit down with your bank statements, a notebook, or a budgeting app — whatever works for you. Write down all your fixed expenses first. Rent or mortgage. Utilities. Food. Insurance. Transport. Phone bills. Subtract those from your income.

Then look honestly at the rest.

Are there any leaks? A subscription you forgot about? Small bits here and there that quietly add up?

Sometimes we tell ourselves we can’t save. But the truth is, we just haven’t looked closely enough yet.

And often, there’s more wiggle room than we initially realise.

The £4,000 Wake-Up Call That Changed My Spending

One of the biggest money leaks in our family was eating out and takeaways.

And honestly, I had no idea.

It wasn’t until I sat down and audited our spending for tax purposes that I saw the actual number. As a family of four, we had spent over £4,000 in a year on eating out and takeaways.

I remember just staring at it.

Before that moment, eating out every weekend had just become normal. It didn’t feel excessive. It felt like just… life.

But seeing that number changed something for me. We still eat out, maybe once a month now, but it’s a choice we make intentionally, not a habit we’re barely aware of.

And that one change alone freed up a surprising amount of money.

This isn’t about never enjoying yourself. It’s just about knowing where your money is quietly disappearing.

Step 2: Start Tiny — Seriously

If money feels really tight right now, start with £5 a month. Seriously.

Open a separate easy access savings account and set up an automatic transfer. Easy access means you can put money in and take it out whenever you need to — which is exactly what you want for an emergency fund.

When it comes to interest rates, it really is worth shopping around. App-based banks like Chase, Plum, and Moneybox tend to offer much better rates than the big high street names — some are paying around 4.75% AER right now (as of writing this article). To find the best current rate, check a comparison site like MoneySavingExpert or MoneyfactsCompare. Just watch out for introductory bonuses — some accounts offer a higher rate for the first year and then drop, so it’s worth keeping an eye on it.

You probably won’t even notice that £5 leaving your account. But you’ll start building the habit. And that habit matters more than most people realise.

I also want to say this, because I wish someone had said it to me earlier — you don’t need to be some incredibly disciplined person before you start saving. Life is busy. People get tired. Motivation comes and goes.

That’s why systems matter more than willpower.

Instead of relying on yourself to remember every month, automate it. Set it up once and let it quietly run in the background. Treat your savings like a bill — something that just goes out, no decision required.

Because every small amount you save is buying your future self a little more peace of mind.

Consider the UK Help to Save Scheme

If you’re on Universal Credit or Working Tax Credit, this is worth knowing about.

The government runs a scheme called Help to Save, and honestly, I think it’s one of the most underused tools available to people on lower incomes.

Here’s how it works. You save between £1 and £50 a month. The government then gives you a 50% bonus on what you’ve saved. The account runs for 4 years, and you can still withdraw money if you really need to.

So if you saved £50 a month, you’d put away £2,400 yourself — and receive up to £1,200 in government bonuses on top of that.

That’s a significant boost just for building a habit you were going to build anyway.

Even if you can only save smaller amounts, you still get the bonus. Every little counts here.

If you think you might qualify, it’s worth looking into it on the GOV.UK website.

Put Your Emergency Fund Somewhere Separate

This one sounds simple, but it makes a real difference.

When your savings are sitting in the same account as your everyday money, it’s too easy to dip into them. You tell yourself it’s just this once. And then it happens again.

Opening a separate easy access savings account creates a little mental boundary. The money is still there if you genuinely need it, but it’s not just sitting there tempting you every time you check your balance.

You want your emergency fund to feel separate. Protected. Like it has one job, and that job is to be there when things go wrong.

And if you can find an account with a decent interest rate, even better. It won’t make you rich, but your money will quietly grow while it sits there doing nothing.

Set Up a Simple Savings System That Runs Automatically

So here is what that actually looks like in practice.

Set up a standing order of £5, £10 or £20 a month automatically moving into your savings account. Decide how much you can realistically put aside and stick to it.

And honestly, most people won’t miss small amounts once the system is set up. You learn to adjust to living on what remains, and your emergency fund quietly grows in the background.

Small automatic savings are far more powerful than big inconsistent ones.

Once that pot starts growing, you’ll feel so proud of yourself and naturally want to save more, because saving has now become part of your normal routine.

Look for Hidden Money in Your Life

One thing I have realised is that there is often money hiding in plain sight.

You just have to look for it.

Negotiate Your Bills

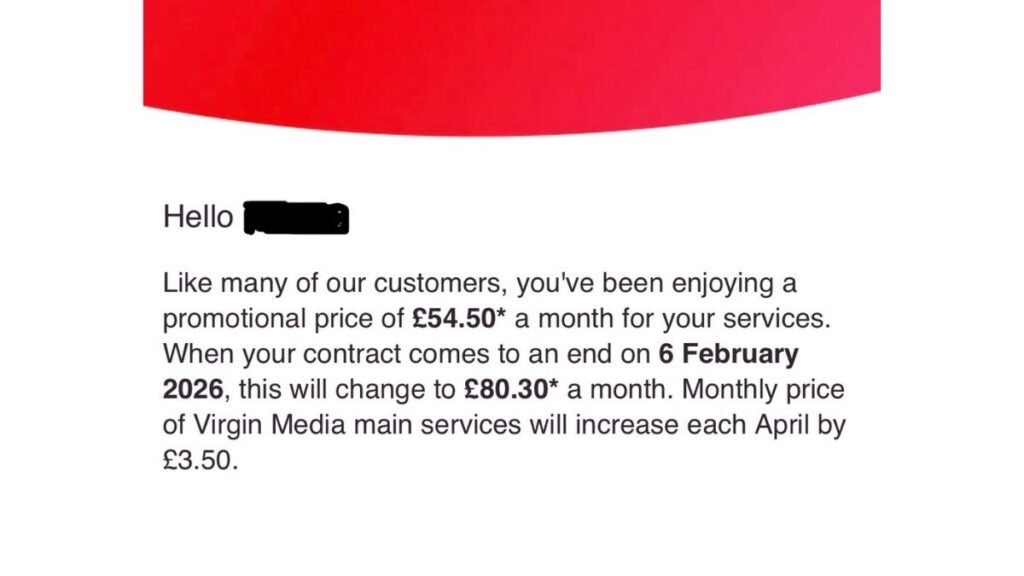

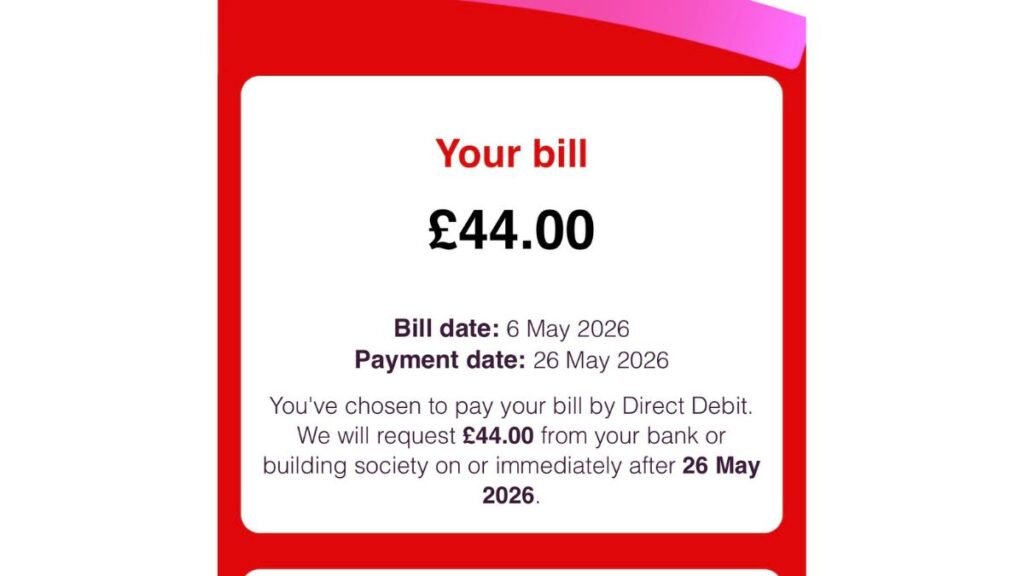

When my Virgin Media contract was coming up for renewal, my bill was about to increase significantly. Instead of just accepting it, I called them and negotiated. I explained that we didn’t even use the landline, and I managed to reduce the bill while also getting Netflix included. Because Netflix was now included, I cancelled my separate subscription too.

That one phone call saved us around £49 a month. That’s nearly £600 a year.

I think a lot of us put off making those calls though. We tell ourselves we’ll deal with it later, and then suddenly the contract auto-renews and we end up overpaying for another year.

Try not to let contracts renew without checking first. Broadband providers, phone companies and insurers spend huge amounts of money trying to attract new customers. In most cases, they would rather keep you at a better price than lose you completely. You often have more negotiating power than you think.

Compare Your Insurance Properly

The same applies to car and home insurance. Before your renewal comes through, compare prices properly instead of automatically accepting the quote. Sometimes switching providers saves a surprising amount for very little effort.

Small savings like these may not feel life changing on their own. But together, they can create real breathing room in your finances.

Check Your Loyalty Accounts and Cashback Apps

If you shop at Tesco, log into your Clubcard account online regularly. Don’t just wait for vouchers to arrive in the post.

Recently I logged into mine and found almost £10 worth of unused coupons sitting there that I didn’t even realise I had. These small amounts add up.

You can also use cashback apps for purchases you were already planning to make anyway. The important thing is intentional spending. Cashback only works if it is attached to money you would have spent regardless.

Consider Bank Switching Offers

Another way to give your emergency fund a small boost is through bank switching offers. Right now, banks like NatWest and First Direct are offering up to £200 in cash for switching your current account using the official Current Account Switch Service.

The switching process is usually much easier than people expect. Things like your direct debits and standing orders are moved across automatically.

Just make sure you read the terms and conditions carefully first. Most offers require a minimum deposit or a certain number of active direct debits to qualify. But used carefully, bank switching can be a genuinely easy way to add a lump sum straight into your emergency fund.

Sell the Things You No Longer Use

I genuinely think many families are sitting on unused items worth more than they realise. Clothes, toys, books, kitchen appliances, baby items. It all adds up.

Vinted is especially easy to use, which is one reason I like it. You simply upload a photo, write a short description and post the item. Even small sales build up surprisingly fast when the money goes directly into savings instead of being spent again.

Most of us have more value sitting around our homes than we think.

Cut Back Ruthlessly on Things You Do Not Truly Care About

One mindset shift that really helped me was becoming more intentional about what actually adds value to my life.

I would rather spend on things that genuinely bring peace, joy or meaning than spend mindlessly just because something feels normal or socially expected. Sometimes we keep expensive things out of habit, not because they truly improve our lives.

Ask yourself honestly. Do I really need this expensive car on finance? Is this purchase genuinely enriching my life? Or is it quietly draining my finances and my mental space?

I think many of us are happier when we simplify.

Cut back ruthlessly on the things you do not truly care about, so you can spend more intentionally on the things you genuinely do.

That is not deprivation. That is alignment.

When you put money aside for your future, you are saying I care about you. And your future self deserves that care.

Your Emergency Fund Does Not Need to Start Big

It just needs to start.

Even a small emergency fund can slowly change how secure and calm you feel about the future. You do not need a perfect income, perfect discipline, perfect timing or perfect financial knowledge.

You simply need to begin.

Start small. Automate it. Stay consistent. Look for leaks. Be proactive.

Little by little, those tiny actions build something much bigger than money. They build confidence.

Your Action Steps Starting Today

- Calculate your baseline and know your numbers

- Look honestly at your spending leaks

- Open a separate savings account

- Automate even £5 a month

- Negotiate one bill this week

- Compare your insurance before renewal

- Check your loyalty accounts for unused rewards

- Consider cashback or bank switching offers carefully

- Sell a few unused items on Vinted

- Focus on progress, not perfection

You do not need to change your entire life overnight.

You just need to start somewhere.

And one day, your future self may look back and feel incredibly grateful that you did.

Related Post:

How to Start Investing in the UK With Just £50 a Month (A Stay-at-Home Mum’s Honest Guide)

10 Beginner-Friendly Finance & Investing Books That Changed How I See Money

Hi, I’m a stay-at-home mum of two based in the UK, passionate about personal finance, intentional living, and building wealth without obsessing over money. I believe investing isn’t just about growing money- it’s about creating more time freedom and the ability to live life more intentionally. Through Mindful Money Growth, I share realistic money tips, mindset shifts, and simple investing ideas for everyday women and mums in the UK.